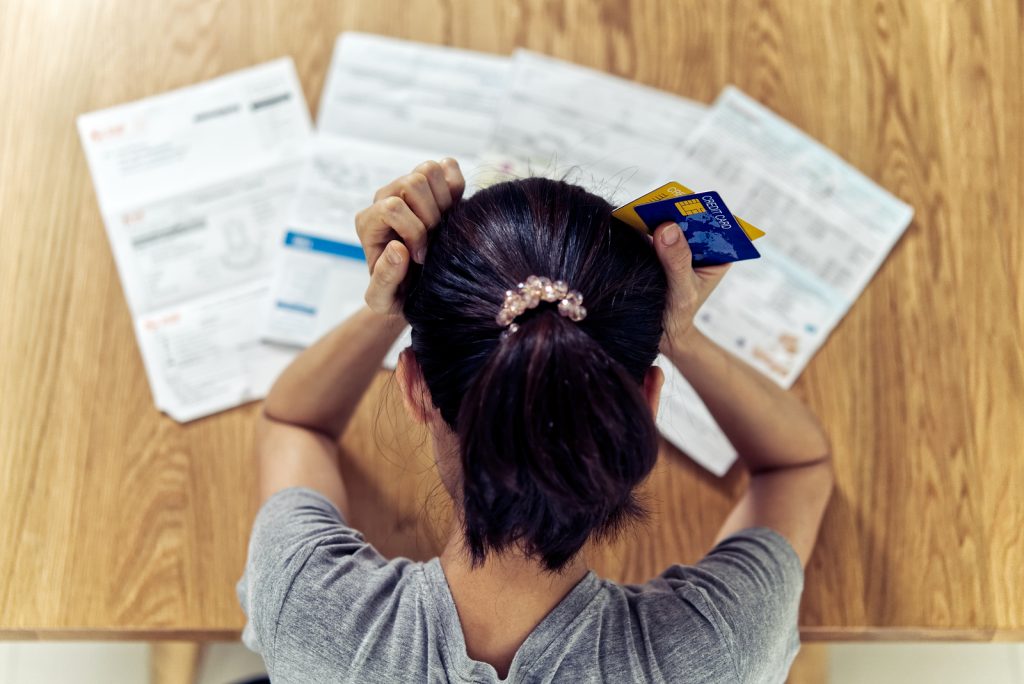

It is a financial rite of passage, but it is also one that must be handled with care. Seeing that first credit card arrive in the mail may be exciting, but it is easy to misuse the privilege and get caught up in a cycle of endless debt.

Like any financial tool, the value of your first credit card is in how you use it. So when that card arrives in the mailbox, take a step back, take a minute and use these tips to steer clear of the debt trap.

Set Spending Alerts

When your new credit card arrives, you will want to set up spending alerts right away. These text or email alerts will help you track and control your spending, but they will also give you early warning of fraud and unauthorized activity on the card.

Once those spending alerts are in place, you can use them to track how much you are spending, making it easier to pay your bill in full when the bill arrives. The more you know about your credit card spending, the easier it will be to avoid the debt trap.

Establish a Spending Budget

It is easy to view your first credit card as a license to overspend, and that is what the credit card companies are hoping for. If you want to disappoint those issuers and avoid high interest charges, start by setting a monthly spending budget ahead of time.

You will probably want to start small, perhaps a few hundred dollars to get you started. Now that you have your spending alerts in place, you can keep a running tally, so you will know when to put that credit card away.

Prepay Your Credit Card Bill

This clever trick is a great way to avoid overspending and steer clear of the credit card debt trap. Now that you have established a spending budget, go ahead and prepay what you expect to charge in the coming month.

When you pay your bill ahead of time, your card will show a credit balance, but that is nothing to worry about. Every time you make a purchase, the money you spend will eat into what you have already paid, and if all goes well you will start the new month with a zero balance.

You can use this strategy as many times as you need to, giving you the training you need to use your new financial tool wisely. As you get a feel for the process, you can stop prepaying, but never stop monitoring your spending. You might even want to set aside cash in a savings account to pay your bill when it arrives.

Request a Credit Line Decrease

This one should be a last resort, but if you are worried about your ability to control your spending, you can always ask that your credit line be decreased. Reducing the amount you can spend on your credit card can be a good way to enforce spending discipline, but it should only be an interim step.

Keep in mind that reducing your credit limit could hurt your credit score. Your credit utilization rate, based on the percentage of available credit you are using, plays a role in determining your score. That potential hit to your credit score is one more reason to view this request as a last resort.

When properly used, a credit card can be a wonderful financial tool, giving you the convenience you need to make online purchases, rent a car, book a hotel room and live a great financial life. But like any tool, a credit card can be misused, and there is a bit of learning curve for new users. Now that you know how to use your credit card wisely, you can pull out your plastic with confidence without paying a penny in interest charges.